Mettler-Toledo Stock: Excellence In Business Economics And Investment Debate (NYSE:MTD)

")

Pgiam/iStock via Getty Images

Investment Thesis

Mettler-Toledo International (NYSE:MTD) is a leading global supplier of precision instruments and services for laboratory, industrial, and food retail applications. Despite facing challenges in certain regions [esp. China], the combo of 1) MTD’s operating model, 2) highly diversified product portfolio, and 3) geographic distribution positions the company to produce sustainable and predictable growth in free cash flows in my best estimation.

Net-net, I reiterate MTD a buy, ~$1,600/share (fair value), based on 1) fundamentals, 2) management’s capital discipline, and 3) valuation.

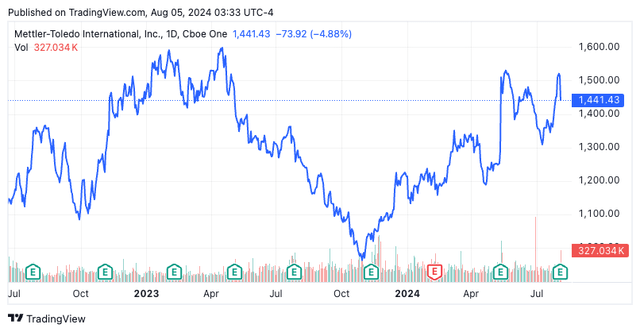

Figure 1.

Tradingview

Investment Update

Following my last publication around twelve months ago, Mettler-Toledo International Inc. shares are -4% but on the path to recovery are a steep selloff throughout ’23. That publication, titled “sell theses missing some key points”, covered several critical facts to the investment debate, namely:

- Pessimistic views of MTD look only to the book value of net assets employed in the company, which, due to its extensive buyback program, are routinely negative. I’d remind readers that accounting values – i.e. book values – demonstrate what’s been put into a firm; economic value illustrates what can be pulled out of it moving forward.

- MTD is a high-quality enterprise that runs on minimal operating assets and has minimal reinvestment requirements to maintain its competitive position and/or grow. The business does not commit to growth to create shareholder value, instead buys back anywhere from $850mm–$1Bn of stock every rolling 12 months. This is highly valuable as it increases our ownership in this high-quality enterprise without committing any extra capital.

- My analysis suggests the business produces ~$700mm-$1Bn in freely available cash every rolling 12m months as 1) it earnings exceptionally high rates on the investor capital put to work in the business [north of 50%], and 2) it’s highly sought-after product lines exhibit consumer advantages [seen in the +23% post-tax margins on sales with >1x capital turnover].

- It reinvests These hard-to-replicate business advantages create a long-term compounding machine whereby the runway for management to deploy capital is extensive because it can just commit to the buybacks. My view is the stock is undervalued, so all uses of capital this way are highly beneficial to shareholders in my opinion.

- Reinvestment rates are <3% meaning the discounted value of freely available cash to a hypothetical private owner of the business after all capital requirements amounts to an implied intrinsic value higher than where MTD trades today on conservative forward estimates. We are in effect getting MTD at a discounted multiple to the value of these economic earnings.

This is a name I am highly familiar with, having owned it in our portfolios here at Bernard for several years and covered it extensively here on SA. See all of the analyses here:

Recent developments

Q2 FY’24 earnings insights

MTD reported Q2 numbers last week and clipped sales of $943.8mm (-2% YoY) mainly due to FX headwinds. China continues to be a drag on performance with sales -21% YoY off a high base in FY’23. Segment growth was flat, with laboratory +1%, industrial -5% and food retail -10% YoY.

It pulled this to operating income of $284mm, down 800bps YoY driven by ~130bps contraction in operating margin. The geographical breakdown was as follows:

- Sales in Europe were +6% underscored by the Laboratory and Industrial segments. Management said it has a higher proportion of sales through MTD’s direct sales force in EU which is driving growth.

- When asked if this success will prompt more investment in other parts of the salesforce, management said “When it comes to investment in sales channel. We are looking at it from a coverage perspective. Do we really cover all the important end markets around the world?…it’s a very differentiated approach we take worldwide of how we look at this. And if we are thinking about investment, it’s, first and foremost, dependent is the underlying market momentum there to increase our sales force.”. I think this is a critical point moving forward and one to look for in future earnings reports.

- Sales in the Americas were +2% despite longer purchasing cycles, which was a positive.

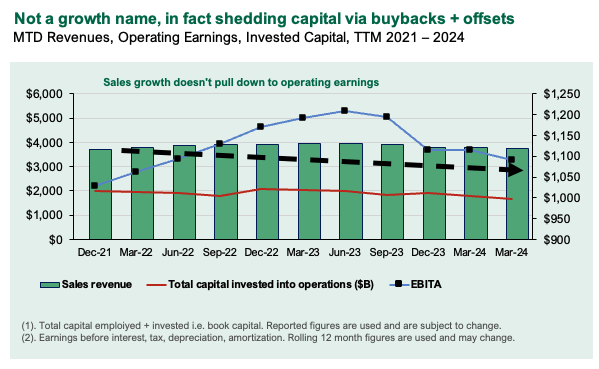

- The major negative continues to be the China drag. Sales were -21% YoY management said the situation was neither worsening nor improving. China has been a drag on the P&L + cash flows for some quarters (Figure 2), so I’d like to see what management’s plans are in addressing this moving forward.

Figure 2.

Company filings, author

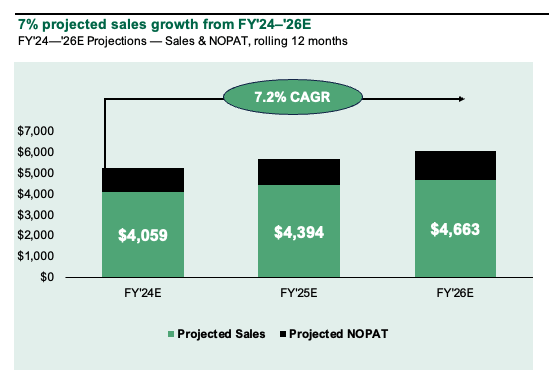

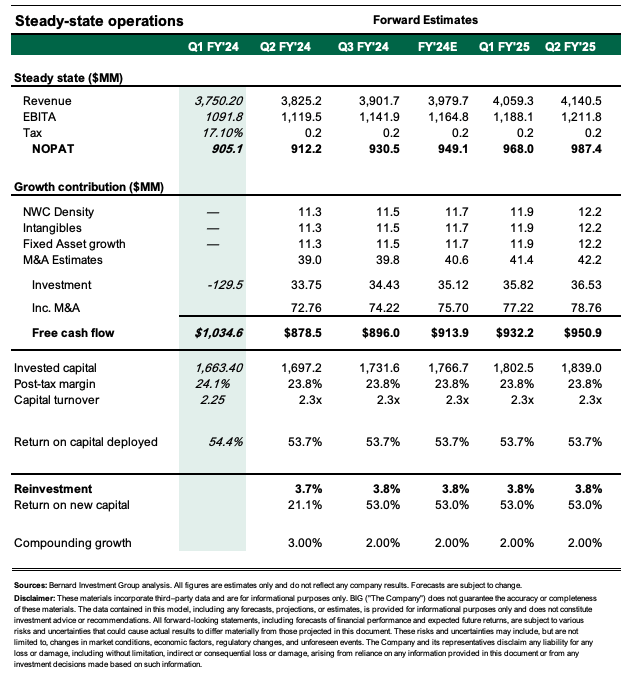

Management forecasts 2% sales growth for FY’24 on earnings of ~$40/share, a slight revision higher from previous estimates. My estimates [see: Appendix 1] have the company to produce ~$4Bn in sales this year [in line with consensus] and ~7% compounding growth to $4.6Bn by FY’26E [ahead of consensus]. I get to ~$850–$900mm in FCF this year – management said it will buy back ~$850mm of stock this year. This is positive in my view.

Figure 3.

Author’s estimates

Attractive valuation with conservative assumptions

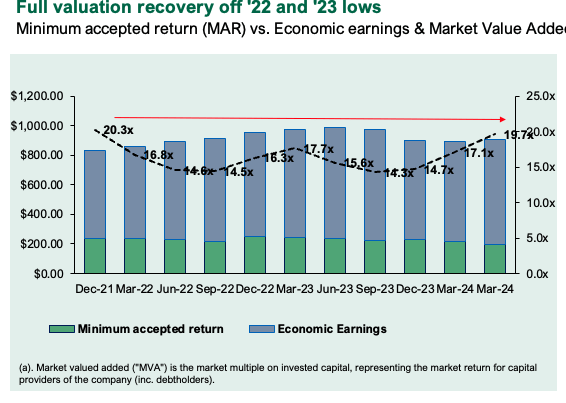

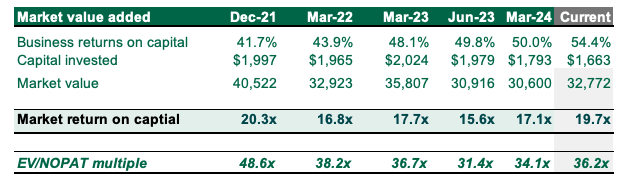

The business runs on ~$1.6Bn of capital invested and is valued ~20x this amount in the market. Investors have bid this from ~14x in FY’22 and FY23 (Figure 4) and now expect ~$31Bn of economic value from MTD moving forward at these multiples ($32.7Bn EV – $1.66Bn IC = $$31.12Bn).

Valuation insights

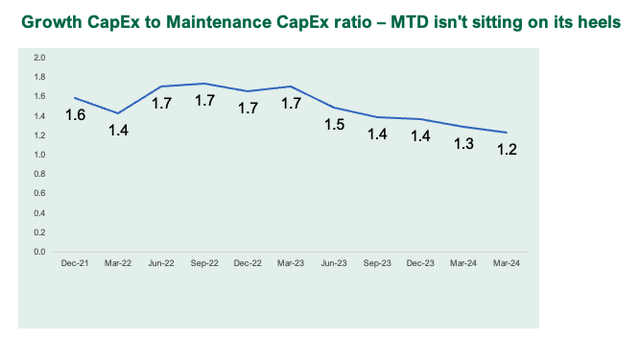

- In my view MTD clearly warrants this multiple range as 1) post-tax margins of ~23-24% on ~2.2x capital turns earn >50% of all the capital running in the business, and 2) it requires minuscule reinvestment of cash flows to maintain its competitive position. As such, against our 12% hurdle rate, MTD produces exceptional value, adding ~$7.5Bn ($340/share) of economic profit since FY’21. Here’s the thing, though – MTD isn’t sitting on its heels. It is investing plenty of cash above its maintenance level of CapEx (approximated as D+A each period). This is highly positive and illustrates management’s stewardship over investor capital (Figure 4.a).

Figure 4.

Company filings, author calculations

Figure 4.a.

Company filings

Figure 5.

Company reports, Author’s calculations

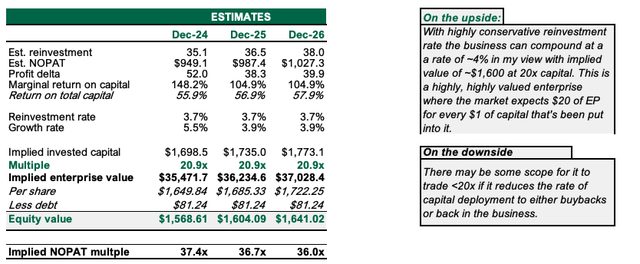

- On the upside, with highly conservative reinvestment rates [<10% of NOPAT] the business can compound at a rate of ~4% in my view, with an implied value of ~$1,600 at 20x capital (Figure 6). This is a highly valued enterprise where the market expects $20 of EP for every $1 of capital that’s been put into it. It warrants this multiple due to 1) the outsized ROICs, 2) the persistence in these for the last 5 years, and 3) the fact ~18% of sales pull through to economic profits every 12mo period [against a 12% capital charge]. A high ROIC firm has more funds to re-deploy, and can thus deploy more [inc. buybacks]. No matter what way you look at it, at a given multiple, MTD has an extensive runway to create shareholder value in my view.

- On the downside, there may be some scope for it to trade <20x if it reduces the rate of capital deployment to either buybacks or back in the business. I place a low probability on this as 1) MTD’s been buying back stock at this pace since the mid-90s, and 2) It throws off ~$700mm-$1Bn in FCF each period.

Figure 6.

Author

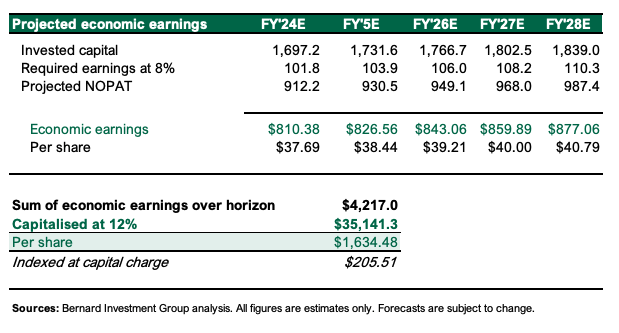

- The discounted value of freely available cash that I believe MTD can produce in the next 5yrs suggests the business could be worth ~$1,600/share as well. Here I’m specifically interested in the cash flows above a 6% comparison rate (the yield on many investment-grade corporates with similar risk characteristics), then discounted at our 12% hurdle rate (representing the opportunity cost of the broad indices). This implied value to a private owner suggests we are buying MTD at a discount to its true intrinsic business worth. This supports a buy.

Figure 7.

Author

Risks to thesis

Downside risks to the thesis include 1) continued China drag on MTD’s sales (this reduces the implied value), 2) investors paying <15x EV/IC (I place low probability on this), and 3) the broader set of macro risks that cannot be ignored right now, namely the selloff in broad markets and what spillover this may have to individual stocks.

In short

MTD continues to present with exceptional economic characteristics by our standard, which support a buy rating, based on – 1) MTD throws off ~$700-$1.Bn in FCF each period which it uses to buyback stock + maintain its competitive position, 2) the highly valuable enterprise providing a long runway to compound, and 3) appropriate valuations that support ~$1,600/share at fair value. Net-net, reiterate buy.

Appendix 1.

Author

link